Everything HR Needs to Know About Lifestyle Spending Accounts (LSA)

Estimated reading time: 6 minutes

Flexibility is one of the biggest challenges facing organizations today. Employees want flexibility and it’s hard to design workplace programs, policies, and procedures with huge amounts of flexibility. This doesn’t mean we shouldn’t try.

For example, I’ve recently seen some articles about lifestyle spending accounts (LSA) and their ability to offer employees flexibility when it comes to their wellness needs. According to CFO Magazine, 75% of large employers offer LSAs to their employees. So, what are lifestyle spending accounts and why would organizations consider one?

To help us understand this new frontier, I reached out to Lindsay Steckler, health and performance manager for HUB International. She has over 10 years of experience in the wellness industry, and a proven track record in strategic planning, program development, and vendor management. Lindsay consults on wellbeing strategies with a wide variety of organizations, ranging in size from 50 to 15,000 employees. She assists clients with data analytics, business planning, incentive design, and program evaluation.

Lindsay, thanks for being here. Can you briefly explain what lifestyle spending accounts (LSA) are?

[Steckler] Lifestyle Spending Accounts (LSA) are a post-tax benefit that allow employees to purchase wellbeing products and services they value most. Not only are LSAs highly flexible but they can be launched at any time helping employers deliver benefits that appeal to today’s workforce.

Unlike individual vendor discounts, wellness stipends provide choice which increases the benefit’s appeal to a geographically and demographically diverse workforce. When employers partner with a vendor administrator, they can offer inclusive perks without spending a lot of money or HR time to do so.

It’s my understanding that LSAs are different from health spending accounts (HSAs). If organizations already offer HSAs, does adding a LSA make any business sense?

[Steckler] LSAs are distinctly different from Health Spending Accounts (HSAs) or Health Reimbursement Accounts (HRAs) in a few ways:

LSAs are funded by the employer only and as a taxable benefit, they’re not subject to nondiscrimination requirements under the Internal Revenue Service (IRS) code. Per the Affordable Care Act (ACA), HRAs must be ‘integrated’ and only those enrolled in medical coverage can participate. If the employer offers a high deductible health plan (HDHP), the HRA would need to be HDHP compliant.

On the other hand, an LSA can be offered to all employees regardless of enrollment because an LSA cannot include medical care. Otherwise, this would make it an HRA. The employer determines eligible criteria for using the LSA and the employer retains any unused funds.

Why would an employer want to offer a lifestyle spending account? What are the advantages for employees?

[Steckler] There are two primary benefits to employees: flexibility and high value.

- Flexibility: The employee determines how they’d like to use the fund (subject to the employer’s criteria).

- High value: Because of this flexibility, these benefits are highly valued by employees.

Benefits to the employer include:

- Flexibility: With an LSA, an employer designates after-tax funds to help employees prioritize wellness activities of their choosing for expenses that aren’t covered by traditional benefits. This ensures that employer dollars are being used in a way that employees value while eliminating the need for multiple point solutions.

- Inclusiveness: Providing flexibility in how the stipend is used allows employers to address benefit gaps and create a more inclusive benefit program.

- Recruiting and retention tool: Lifestyle benefits like wellness stipends demonstrate to employees that their employer cares about them as a person, not just a worker.

- Employee appeal: LSAs allow employees to spend on a broad range of wellness needs regardless of where they live or work, making them a great option for supporting the modern workforce.

When employees feel cared for, employee engagement and productivity improve, and employers enjoy lower rates of absenteeism and turnover. Additionally, since LSAs are not subject to nondiscrimination rules, an employer can use the funds to recognize service milestones for a specific class of employees (Example: recognizing call center workers after 12 months of employment).

Are there any disadvantages or concerns that employers need to consider when it comes to lifestyle spending accounts?

[Steckler] There are two areas that organizations should be cognizant of when it comes to LSAs: benefit design and compliance.

On the compliance side, LSAs cannot cover ‘medical care’. Beware of expenses such as therapy sessions, chiropractic care, and acupuncture which are likely to be medical care (although not always) and expenses such as vitamins, massages, and gym memberships can also be medical care (though less common). The same applies for travel (medical travel = medical expense).

There’s also the concept of constructive receipt, which is a tax term that determines when an individual has received income. Constructive receipt occurs when an individual obtains income that is not yet physically received but has been credited to the taxpayer’s account and over which they have immediate control. This places heavy restrictions and requirements on employers seeking to give employees a choice between taxable and non-taxable benefits (i.e., offering an LSA or HRA). It can be triggered when an employer allows an LSA balance to rollover and make income taxable in the year it becomes available.

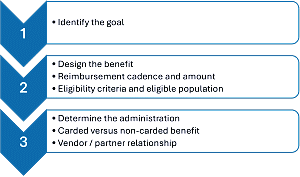

The other consideration is benefit design. Employers need to be aware that structuring the benefit as a reimbursement may unintentionally discriminate against employees who do not have the funds available for the purchase. It’s important to approach the LSA program design strategically: identify the goal, design the benefit, and determine the administration.

Last question. You mentioned earlier that LSAs can be launched at any time. Since many organizations have already done their open enrollment for the year, how easy is it to set up an LSA mid-year?

[Steckler] LSAs can be launched at any time (and therefore terminated at any time, pursuant to administrative vendor contracts).

Most employers set an annual cap of $500-$1,000/per employee. Each LSA can have its own design, eligible population, dollar amounts, funding frequency, reimbursement processes, and spending timeframe. This is a highly utilized benefit this should be considered when organizations budget for this benefit.

I want to extend a huge thanks to Lindsay for sharing her knowledge with us. If you’re looking for ways to make your benefits more flexible, check out HUB International’s Outlook 2024 report. Not only does it talk about ways to strengthen the employee experience, but it outlines opportunities to mitigate risk.

Wellness and wellbeing programs are tremendously popular and for obvious reasons. However, there are recent studies indicating that they might not be as effective as they sound. The reason? They’re not tailored to meet individual needs. What this means is that organizations need to find ways to build more flexibility into their benefits programs. This results in the organization using their resources wisely and employees using the benefit the way they want and need to.

Image captured by Sharlyn Lauby at the SHRM Annual Conference in New Orleans, LA